AGNC Investment decision: Not Out Of The Woods Yet Soon after Jackson Gap (NASDAQ:AGNC)

")

Table of Contents

benedek/iStock by using Getty Illustrations or photos

Thesis

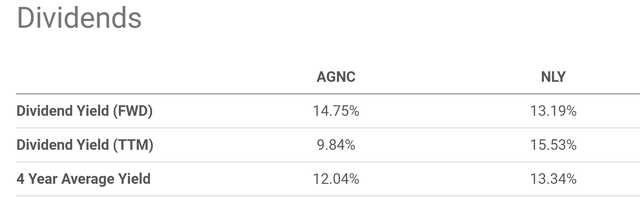

Profits-oriented buyers have good factors to like AGNC Expense Corp. (NASDAQ:AGNC). This home finance loan true estate financial commitment have faith in, or mREIT, inventory now delivers a dividend generate as superior as 14.75% on an FWD basis. And to sweeten the offer, its dividend payouts had been manufactured every single thirty day period. This sort of a generate is not only considerably higher than other solutions (this sort of as high-generate bonds) but also increased than its near friends and its personal historic track record. As seen in the chart below, its shut peer, Annaly Funds Management, Inc. (NLY), now yields 13.19%. And its 4-year typical produce is about 12.04%, about 19% underneath its existing FWD generate. Therefore, judging by the dividend yields, the stock is at present trading at a substantially discounted valuation.

Source: In search of Alpha

Despite the earlier mentioned draws (superior produce and possible valuation lower price), the thesis of this report is to review the possible threats. The mREIT sector is a sector that is quite sensitive to interest fees and as a result my analysis will concentrate on the impacts if the recent desire prices persist, which is a very possible state of affairs in my mind based on Fed Chair Powell’s speech at Jackson Hole last Friday. In the speech, Powell mentioned that inflation is currently “as well significant” and cautioned the current market that the FED is “prepared to increase prices additional.”

In the remainder of this article, I will reveal why the existing fascination premiums are significant plenty of to create strong headwinds for AGNC, permit alone a additional improve. Much more precisely, I will elaborate on the challenges from three areas: AGNC’s price of money, its leverage, and profitability.

Rising charge of cash and unfavorable financial return

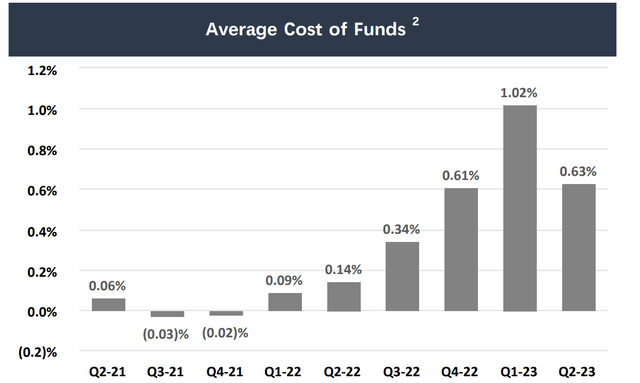

As most mREIT buyers presently know, this sector tends to make its financial gain on the distribute amongst quick-expression borrowing premiums and very long-term lending fees. As the Fed keeps the small-time period fees (which is what the Fed can basically regulate), the cost of resources stays at an elevated level for AGNC, as you can see from the adhering to chart (taken from its Q2 2023 earnings report, ER). It enjoyed basically zero value of money amid the epic quantitative easing soon just after the pandemic broke out. It truly received compensated to borrow dollars during Q3 2021 and Q4 2021 as the price tag of money grew to become slightly destructive.

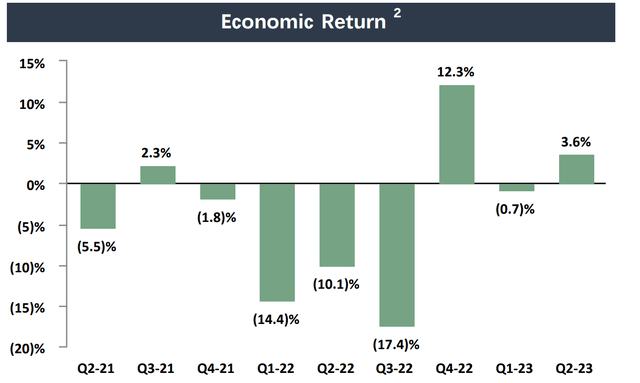

Nonetheless, as the Fed reversed its gears and started off financial tightening, its value of cash stored climbing up. In tandem, its economic returns tanked, as you can see from the second chart beneath. Up coming, I will make clear that the rising borrowing cost is not the only headwind that AGNC will encounter, and the negative economic return could build worse implications than on the area.

Resource: AGNC Q2 ER Supply: AGNC Q2 ER

Housing affordability and profitability headwinds

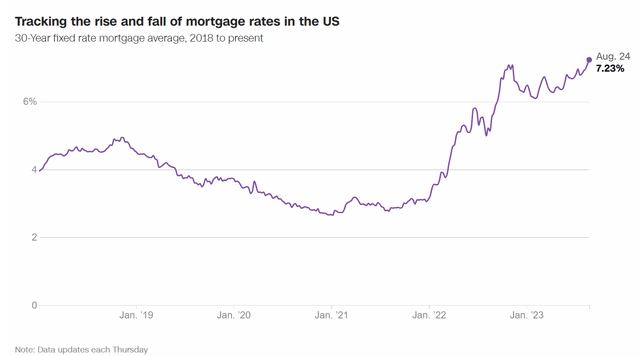

As aforementioned, soaring Fed fund premiums have prompted AGNC’s borrowing charge to rise drastically already. Nonetheless, this is not the only way that a bigger charge could damage AGNC’s profitability. As treasury charges persist at a greater level and with a excellent opportunity for further hikes, mortgage fees are now at a multi-calendar year peak amount. To wit, the chart beneath displays that at the moment, the 30-calendar year fixed level greater to 7.23%, the maximum degree given that at minimum 2018. In my check out, these types of house loan charges are superior ample to seriously suppress refinance and origination activities, producing a sturdy headwind for the mREIT sector and AGNC.

Supply: CNN.com

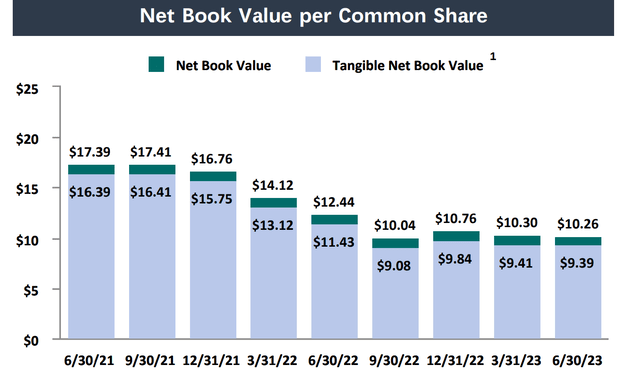

Loss of book price

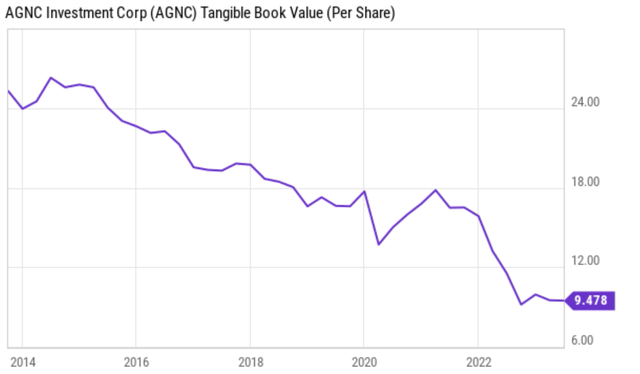

Also, as just described, the detrimental economic return proven earlier mentioned is even worse than on the area. As clarified in the footnotes from the ER, the financial return is described as “the improve in tangible net e-book benefit for every common share furthermore dividends per frequent share declared.” As a outcome, if the tangible book benefit (“TBV”) continues to be, then a declining economic return just usually means declining financial gain, and it hurts traders “only” at the time. But if the TBV also declines at the similar time, then a shrinking financial return is worse than on the floor. And that is precisely the case with AGNC as witnessed in the next chart. Its TBV has been in steady decline in new years, shirking from $16.39 per share in June 2021 to the present amount of only $9.39 per share. Broadening our horizon does not change the picture. As seen in the next chart below, its TBV loss is serious in the long term, also.

Supply: AGNC Q2 ER Resource: Searching for Alpha

Other pitfalls and final views

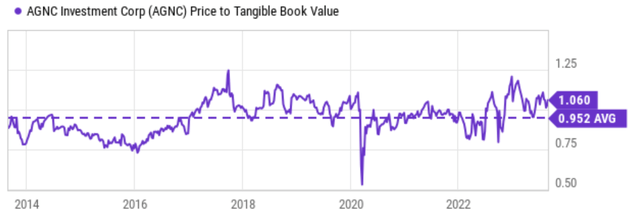

Besides the higher than problems, there are a couple of other dangers worth mentioning. As described before, judging by the dividend yields, AGNC is presently trading at a valuation price cut. Nevertheless, other metrics ship a combined sign. For instance, the next chart exhibits its valuations in conditions of the P/TBV ratio. To wit, its ordinary P/TBV ratio has been about .95x traditionally. The recent P/TBV ratio of ~1.06x is in fact about 10% higher than the historical common.

Supply: In search of Alpha

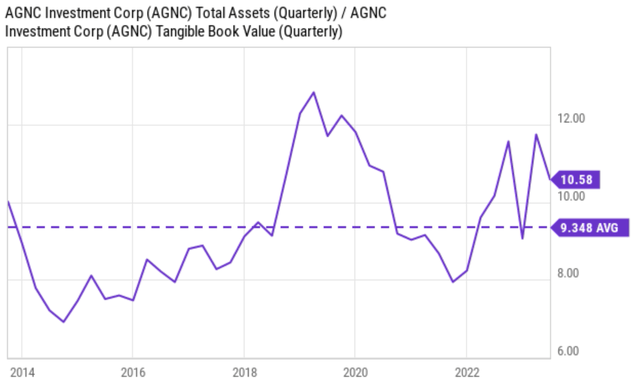

Its leverage is one more worry. As witnessed in the subsequent chart under, AGNC started deleveraging in 2020, in all probability sensing that the rock-bottom fascination costs will never previous for too long. Its leverage (in conditions of complete asset/TBV) decreased from an alarming stage of ~13x to a amount of close to 8x by late 2021. Having said that, its leverage has climbed back considering that then and now hovers about 10.6x. It is considerably over its average level of 9.3x in the previous 10 yrs, and bear in brain that the present-day desire charges are higher than the common in the earlier 10 several years.

Supply: Searching for Alpha

All advised, there are great causes to like AGNC. Its 14%+ generate is higher than most solutions, shut friends, and also its personal historical common. My thesis, nonetheless, is to position out the risks. My essential considerations with AGNC Expenditure Corp. are threefold: charge of resources, leverage, and profitability. As thorough higher than, I am worried that its profitability will be damage in numerous ways if the benchmark price persists at the latest degree or even more will increase (which is possible primarily based on my reading through of the message from the Jackson Gap assembly). Borrowing expenditures would continue being higher or even additional climb and desire for new home finance loan or refinancing would soften. These troubles could also trigger further more TBV erosion, each pressuring its inventory rates (specially thinking about the recent P/TBV a number of is higher than the historical normal) and shrinking its money foundation to make earnings.