This financial commitment move could bring about a huge Medicare penalty

If you’re in your 60s or more mature and earning sizable Roth conversions, it is not just cash flow taxes that you want to stress about. You might also bring about a lot increased Medicare Element B and Section D premiums.

We’re conversing below about these Medicare surcharges recognised as IRMAA, quick for profits-similar regular monthly adjustment volume. These surcharges are about and higher than 2023’s typical $1,979 for each person Medicare quality, and they’re based on profits from two several years previously.

IRMAA’s value impact is commonly talked about in terms of regular monthly for every-particular person dollar amounts. But to give audience a far better handle on the legitimate price tag, I have transformed IRMAA’s 2023 surcharges into anything more akin to marginal profits-tax fees.

IRMAA surcharges could volume to about 1% or 2% of total earnings. But which is the regular rate. What I’m concentrated on listed here is the marginal rate. As you’ll see in the tables under, I have calculated “tax-proportion equivalent” IRMAA prices for each single and married taxpayers. These exhibit that the marginal IRMAA surcharges are a least 3% to 5% of the supplemental cash flow involved—but that assumes you’re close to the major of each IRMAA earnings bracket.

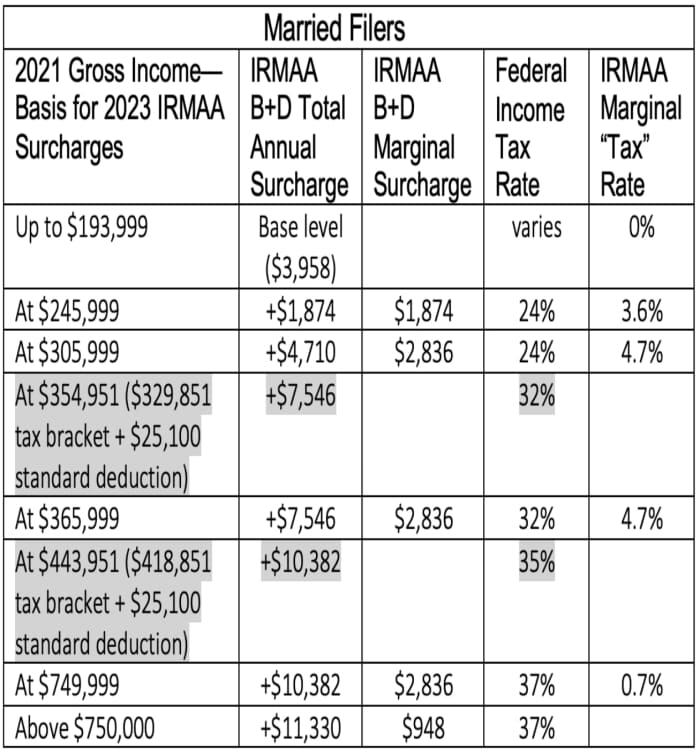

Resource: Humble Dollar

Suppose you are single and your 2021 modified adjusted gross cash flow (MAGI) put you at the prime of the to start with 2023 IRMAA bracket, which is $97,000 to $123,000. You’d shell out a surcharge of $937 in 2023. That surcharge is equivalent to 3.6% of the full dollar bracket quantity above $97,000. Set an additional way, this 3.6% price assumes your earnings was just shy of $123,000.

What if your revenue was under the bracket maximums? The marginal surcharge “tax” charge will be even larger than 3% to 5%—and it could be vastly larger. How occur? IRMAA is a so-called cliff penalty, which means the comprehensive surcharge for any bracket is levied as shortly as your earnings crosses that bracket’s threshold income. In other phrases, IRMAA surcharges for each earnings bracket behave entirely in contrast to typical income taxes, wherever the same marginal tax fee applies to each and every dollar inside of that income-tax bracket.

Source: Humble Greenback

The tables also spotlight two federal revenue-tax thresholds, which are shaded in grey. For instance, the 2021 revenue-tax brackets incorporated a sharp leap in marginal tax charge from 24% to 32% for single filers with taxable cash flow of $164,926 and above, and for joint filers at $329,851 and over. In the tables, these revenue thresholds are altered for the standard deduction, so they are comparable to the IRMAA thresholds. Trying to keep an eye on this kind of federal money-tax thresholds can be as significant as taking care of your IRMAA brackets.

Taking into consideration Roth conversions and anxious about IRMAA? Here are seven insights that my wife and I have gleaned:

- The tables clearly show a powerful incentive to undertake Roth conversions in advance of age 63. The moment you get to 63, any Roth conversions could most likely impact the Medicare premiums levied two several years afterwards, when you transform age 65. With the reward of hindsight, my wife and I really should likely have done larger conversions prior to age 63.

- We regulate our cash flow, which includes prepared Roth conversions, to place us towards the major of our IRMAA earnings bracket, so the marginal surcharges are in the 3% to 5% assortment.

- Whether you’re changing to a Roth or not, there is a enormous incentive to continue to keep your money from breaching the future IRMAA earnings threshold. In point, IRMAA surcharges at the commencing of brackets might be the country’s most punitive incremental tax, which—for a married couple—I calculate to be some 28,000,000% on that 1st penny.

- IRMAA brackets two a long time from now aren’t acknowledged exactly due to the fact the thresholds are inflation-adjusted. Still, early projections are available. We manage our earnings to get within just $4,000 to $5,000 of the projected bracket ceiling, consequently leaving some margin for error.

- When expected minimum distributions kick in, we’ll most likely come across we’re even now in IRMAA surcharge territory. Still, today’s conversions should really assist, because subsequent financial commitment advancement from today’s Roth conversions will never result in IRMAA.

- Federal earnings-tax brackets are also really worth watching, particularly individuals at 2023 taxable incomes of $182,100 for single filers and $364,200 for married filers. These induce the eight-percentage-issue leap to the 32% revenue-tax level. In recent decades, the revenue amounts the place tax prices bounce have frequently been near to one particular of the IRMAA bracket ceilings.

- IRMAA surcharges are a single-yr price. But the Roth conversions that set off that charge will outcome in many years of tax-no cost growth for us and our heirs, and that advancement ought to assist us recoup today’s IRMAA costs.

This column 1st appeared on Humble Greenback. It was republished with authorization.

John Yeigh is an author, speaker, coach, youth sports advocate and businessman with much more than 30 years of publishing practical experience in the athletics, finance and scientific fields. John retired in 2017 from the oil business, in which he negotiated fiscal details for multibillion-dollar global tasks. Check out his earlier articles.