My 33 Investment decision Several years | Morningstar

Table of Contents

The Acorn

When I begun working at Morningstar (MORN), on Feb. 15, 1988, the mood was subdued. Reeling from stocks’ 22% loss on Black Monday (which remains the greatest single-working day drop in U.S. inventory-marketplace history), investors feared the excellent instances were in excess of. Both equally fairness and bond selling prices experienced liked a splendid five-calendar year run from 1982 via mid-1987. Now, it appeared, normalcy would return.

Rather, the rocket ship arrived. The inventory marketplace went virtually straight up, yr soon after calendar year, with inflation and desire fees heading down. The fund small business followed suit. Historically one thing of an investment backwater–coming into the 1980s, the industry’s once-a-year revenues were below $500 million–mutual money strike the mainstream. It was all pretty enjoyable. I was significantly happy due to the fact shortly just after signing up for the business, I experienced disregarded the skeptics and put anything I had (not substantially) into a absolutely invested stock fund.

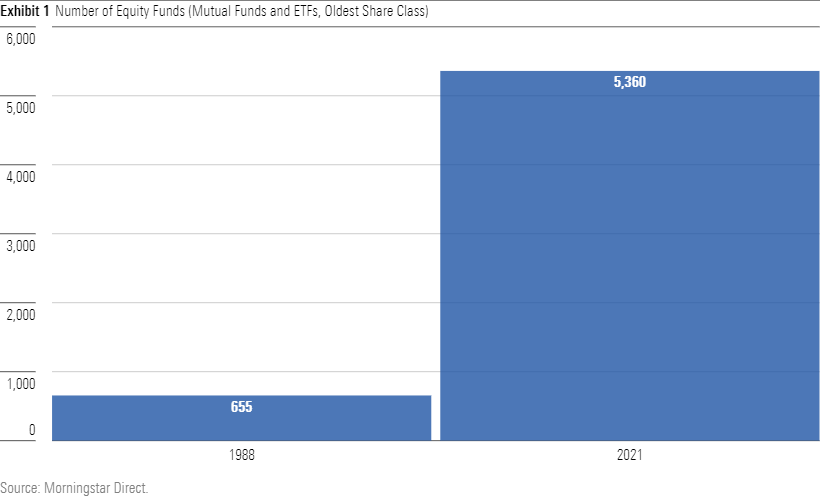

In the early years, Morningstar analysts wrote reports on every present stock fund, including the $5 million Valley Forge Fund, operated by a partner-and-spouse crew. (“Bernie just can’t come to the phone now. Can I have him phone you back, after he finishes mowing the lawn?”) Attempting the same feat today would demand a a lot much larger study crew. Which includes trade-traded cash, the fairness fund rely has octupled.

Income, Dollars, Funds

Whilst spectacular, the boost in the selection of money has greatly lagged the surge in fund property. In 1988, the premier mutual fund was Franklin U.S. Govt Securities (FKFSX), which completed the 12 months with $11.7 billion. (Close behind was a different bond fund, Dean Witter U.S. Govt Securities Believe in (USGAX), which has since been renamed following its present-day proprietor as Morgan Stanley U.S. Govt Securities.) Right now, 348 mutual money and 124 ETFs exceed that determine.

The next chart, contrasting mutual-fund assets in 1988 with people for 1) mutual resources and 2) ETFs in 2021, effectively conveys the tale. When I initially arrived at work, the industry’s progress experienced only just begun.

Sure, all those numbers are not inflation-modified, but executing so would just bump the 1988 determine to $1 trillion. That first yr would nevertheless hardly sign-up on the chart.

The Index Revolution

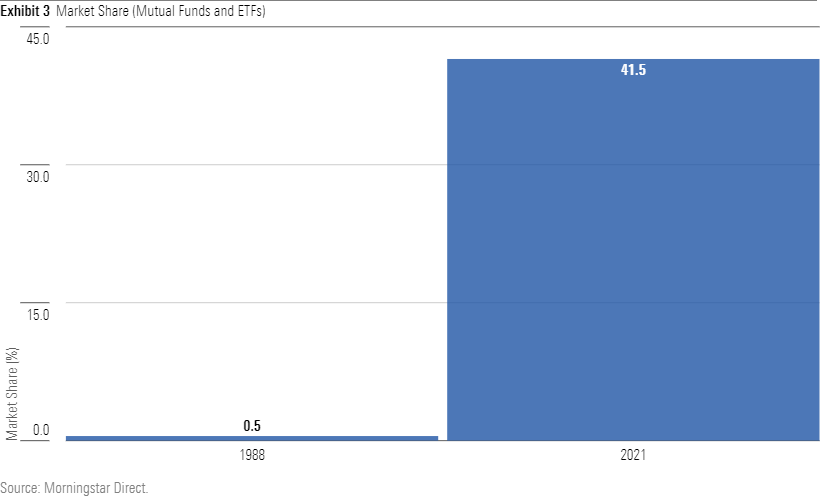

Moreover amazing expansion, the other outstanding fund growth has been the triumph of indexing. In 1988, three index funds existed: 1) Vanguard 500 Index (VFINX), 2) DFA U.S. Micro Cap (DFSCX), and 3) a brand name-new entrant from Fidelity that was ultimately merged into the company’s present providing Fidelity 500 Index (FXAIX). (Even that listing is suspect, as DFA now states that its funds are actively managed. However, as it called DFA U.S. Micro Cap an index fund at the time, that is the place I have positioned it.) In aggregate, individuals money held $2 billion, earning for a market place share of a little beneath .5%.

Right now, index cash account for a lot more than 50 % of fairness fund assets and just more than 40% of the general sector. That percentage surpasses my seemingly rash prediction from the early 1990s that indexers could inevitably management 30% of the fund business, which I experienced flippantly offered to a Dollars reporter. That became the story’s primary quote. Lively administrators have been, shall we say, unamused.

The Value Is Suitable

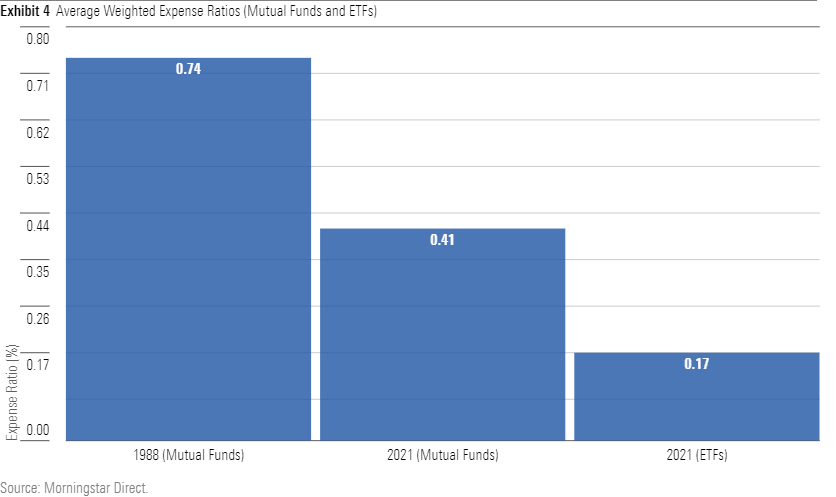

Accompanying index funds’ advance has been better awareness of fund expenditures. Back in the working day, investors who emphasised fund expenses were considered as cranks. Life was far too brief to fret about a couple basis factors. In 1993, for case in point, the 5 leading-selling mutual cash carried normal an average expense ratio of 1.09%. When functionality was sturdy, rate was not a barrier.

That attitude has sharply altered, as reflected not only in today’s best-seller lists– which are dominated by index funds–but also in the industry’s regular greenback-weighted expenditure ratio, which displays wherever traders now keep their monies. That has dropped sharply, from .74% for all stock, bond, and allocation resources in 1988, to .41% for mutual cash now, and a piddling .17% for ETFs. Whereas both immediate investors and economical advisors when downplayed the importance of selling price when assessing funds, they now position expenditure ratios entrance and center.

Admittedly, the all-in prices for fund traders haven’t dropped as substantially as the quantities would look to suggest. Today’s monetary advisors are compensated otherwise. Whereas they as soon as ended up almost solely paid by fund corporations, which embedded product sales prices into their solutions, advisors now mainly charge asset-based mostly expenses. Thus, lots of fund investors pay out extra than the figures propose. On the other hand, their pursuits now align with their advisors’. For just about every party, the less expensive a fund, the greater.

In truth, now that they have grow to be price cut customers, economic advisors like applying institutional shares. Following all, why really should their clientele pay much more, when advisors can use their insider position to set up much better promotions? That the market has come to be so substantial, with well known advisors placing tens of millions of bucks with a one fund group, has strengthened their negotiating electrical power. As a outcome, fund firms have more and more created their institutional shares available to all.

Glory Days

The fund industry’s growth enormously benefited Morningstar. My career has hence been blessed. Although most men and women from my generation have not savored related doing the job situations, all were granted the exact same fantastic expenditure opportunity. The fund enterprise was not alone in outstripping anticipations. So, too, did stock and bond performances, which conveniently outpaced inflation. People who held bonds profited. People who held equities fared much better yet. A lot of turned wealthier than they ever would have imagined. The chart under gives the aspects, for the 33.5 several years that have passed because Aug. 1, 1988.

Irrespective of whether the approaching generation will delight in equivalent expenditure achievements stays to be seen. The consensus is otherwise. Most institutional researchers anticipate the after-inflation returns for the two equities and bonds over the next one particular 3rd of a century to tumble much quick of what the most-new third shipped. That could perfectly manifest I do not argue with the forecasters. However, it is worthy of remembering that when my particular journey began, the smart previous heads sounded the exact same be aware. As Yoda would say, completely wrong they have been.

Delighted holidays, and might your fortunes be as generous as mine have been.

Editor’s Observe: The reference right after Show 2 to the 1988 figure was corrected to trillion, not billion.

John Rekenthaler ([email protected]) has been investigating the fund sector due to the fact 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s financial commitment research department. John is quick to point out that whilst Morningstar ordinarily agrees with the sights of the Rekenthaler Report, his sights are his possess.