Is TQQQ ETF A Better Long-Term Or Short-Term Investment?

Table of Contents

pookpiik/iStock via Getty Images

I was recently asked what the story was with ProShares UltraPro QQQ (NASDAQ:TQQQ). At the time, all I knew about it was that it was a leveraged ETF which allows investors who don’t have margin accounts to boost their gains or losses in the Invesco QQQ ETF (QQQ) by a factor of three.

I had read reports posted in online forums of investors making hefty profits with TQQQ. But I also knew that Vanguard hasn’t allowed investors to buy TQQQ or any other leveraged ETFs on their brokerage platform since January of 2019. They explained they banned this kind of trading as it was too risky for the buy and hold investors the company supports.

As could be expected, that prohibition has made leveraged ETFs like TQQQ more attractive to a certain kind of investor who assumes they are being barred from making certain investments because Wall Street wants to keep all the really good stuff for themselves.

So what’s the truth of the matter? Is TQQQ a way for the little guy to make big money, or is it just another much too risky get-rich-quick mirage that will leave naive retail investors hurting?

What Is A Leveraged ETF?

The unique selling proposition behind leveraged ETFs is that for a relatively high fee you can invest a small amount of money in a stock index and earn a much bigger return than you would get if you put the same amount of money into a regular, unleveraged ETF that tracked the same index. Not only that, but you can do this without needing to be approved for a margin account or indulging in any kind of complicated investing strategy. Just buy the ETF and let the ETF provider work the Wall Street magic that gives you two or three times as much return as you’d get if you just bought a plain vanilla index tracking ETF.

TQQQ is a 3x leveraged ETF. It is as highly leveraged as the SEC currently allows any ETF to be. TQQQ’s stated goal is to deliver three times the daily gain or loss of QQQ. There is however no guarantee that you will actually achieve this result, though TQQQ appears to have delivered on that promise most of the time over the relatively short time they have been in operation. TQQQ only started trading in 2010.

You pay for the privilege. Leveraged ETFs are expensive. ProShares tells us that TQQQ’s effective expense ratio is 0.95%, though it also states its gross expense ratio is higher at 1.01%. This difference may represent a temporary fee concession offered to attract more investors. This is five times the 0.20% expense ratio of QQQ.

There are other, hidden expenses that are a byproduct of the way that TQQQ achieves its leverage. Besides paying the expense ratio that reimburses the fund company for providing the ETF, leveraged ETFs also bear the costs of the derivative trading that provides their excess return, the costs of daily rebalancing of its holdings, and the costs of maintaining the large amount of low yielding very short-term bonds they hold to provide the cash needed for all their buying and selling.

TQQQ’s Rewards Are Obvious

You can’t discuss leveraged ETFs for more than a few minutes before the term “risk” shows up. Everyone acknowledges they are very risky. But investors know that high risks often result in equally high rewards. That has certainly been the case with TQQQ. We’ll look at those rewards first, before probing more deeply into the specifics of the risks that come with pursuing them.

Investors Buy And Hold TQQQ Long-term Because Doing So Provided Extremely High Returns During The Tech Bull Market

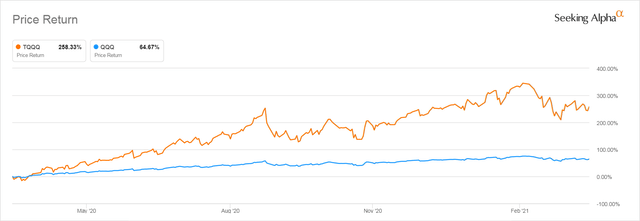

Investors who bought TQQQ just after QQQ hit its lowest price in March 2020 and who held it for exactly a single year achieved a remarkable return, earning 258% on their original investment. That return dwarfed the already impressive 64.67% return of the plain vanilla QQQ ETF over the same period.

TQQQ and QQQ 1 Year Return Starting March 26, 2020

Seeking Alpha

In A Strong Bull Market TQQQ Delivered More Than 3x Returns

The outsized long-term gain TQQQ made over a year-long period are striking, especially in view of the fact that ProShares warns investors very strongly that TQQQ should only be held for a single day and that its results compound in an unpredictable way if held longer than a single trading day due to the ETF resetting daily and the impact of leverage compounding.

Obviously, in a raging bull market like the one that QQQ experienced after March 2020 the “unpredictable” compounding greatly increased the share price. The price return on TQQQ was almost four times that of QQQ, not the three times that ProShares aims to provide the day trader.

But given that ProShares insists so strongly that TQQQ is only meant to be used by day traders, you might ask, why am I even bothering to show the return of TQQQ over an entire year?

The reason is simple: despite the warning, many retail investors have been making long-term buy and hold investments in TQQQ and other highly leveraged ETFs at least since 2019.

Hedgefundie’s Excellent Adventure Popularized Buy And Hold Investing In 3x ETFs

It was in 2019 that news of a supposedly safe way to use 3x leveraged ETFs strategy began to spread around the many investing communities on the internet. The strategy was called Hedgefundie’s Excellent Adventure, which was usually abbreviated as HFEA. The strategy first emerged in a forum post written by someone who called himself Hedgefundie and spread around the internet, and immediately provoked a lot of discussion. Interest in the strategy grew during the COVID-19 lock downs when a generation of young people, discovered how much money could be made, quickly and easily, by using leverage in a market where “stonks can only go up.”

If you have nothing better to do for the next month or two, you can read the more than 15,000 posts discussing the HFEA strategy in excruciating detail on the Bogleheads Forum.

The HFEA strategy as first stated used a different 3x ProShares ETF, the ProShares UltraPro S&P500 (UPRO). This is another 3x leveraged ETF like TQQQ, but it tracks the S&P 500 index, rather than the Nasdaq 100 Index that QQQ tracks. As the COVID lockdowns juiced up the profits of QQQ’s Tech stocks, TQQQ’s return accelerated and exceeded those of UPRO. This convinced many investors to go all in with TQQQ. Seeking Alpha’s Flows page for TQQQ tells us that over the past three years TQQQ’s assets under management have increased by a whopping 374.75%.

The potential return of TQQQ is thus very obvious. There is also a reciprocal risk that is equally obvious.

When Stonks Go Down TQQQ Goes Down A Whole Lot More: The Best Understood Risk Of Leveraged ETFs

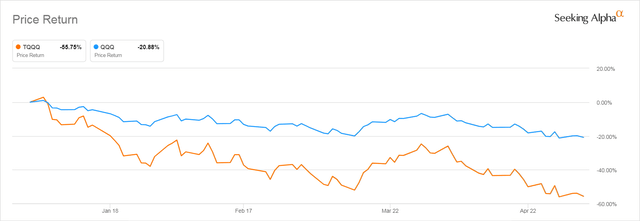

Below you see the return of TQQQ since the beginning of 2022. Though not quite 3x the already painful 20.88% loss of QQQ, TQQQ’s loss of 55.69% was devastating for anyone who invested at the beginning of 2022.

TQQQ and QQQ Return Since Jan 2, 2022

Seeking Alpha

HFEA Investors’ Hedging Failed Miserably

HFEA’s claim to be a safe way to invest in 3x leveraged ETFs was based on the idea you could buffer potential losses by also investing in a second 3x leveraged ETF, the Direxion Daily 20+ Year Treasury Bull 3X Shares ETF (TMF), which leveraged a bet on a long Treasury bond index.

The idea was that the long bond was likely to move in the opposite direction as the stock index if stocks fell because that was what had usually happened during past market declines. Decades of academic backtesting had indeed found that the price movements of long bonds were either uncorrelated or inversely correlated with those of stock indexes. Unfortunately, HFEA investors, like most of us, had only a fuzzy understanding of what the statistical term “uncorrelated” really means.

As HFEA investors have now learned, bonds being uncorrelated with stocks did not mean that they would move in the opposite direction of stocks. In statistics, “uncorrelated” simply means that two numbers will move in ways that aren’t linked to each other in a predictable way. Uncorrelated bonds have mostly gone up when stocks go down over the past 40-year bull market in Bonds, but there is no reason they have to keep on doing that. Since January 2022, in fact, Treasury bonds have dropped just as much as stocks have, sometimes more. The 3x leveraged 30-year Treasury ETF, TMF, is down 50.48% YTD almost as much as is TQQQ. That’s because rates were consistently falling during most of the backtested period. Now they are consistently rising.

Lesson Learned: There is no safe way to make triple returns with leveraged ETFs.

The Other Lesson Learned: Backtesting works great until the conditions change that explain your backtested results.

I mention these lessons because they are relevant for those who rely on TQQQ’s backtested results.

The Lessons Investors Have Taken From TQQQ’s Recent Rise And Fall

Despite its recent collapse, investors who invested in TQQQ early enough to get a good piece of that 258% gain are still ahead on their original investment even after losing 55%, which is why the strategy of investing in TQQQ still appeals to many investors. You will find them on Bogleheads and other internet venues urging others to continue to follow their passive buy and hold strategy, as they assume that QQQ will resume its relentless move upward if they are just patient. They believe that the eventual outsize profits they will make when upwards momentum resumes will make up for their temporary losses.

Other investors, including some authors who are publishing articles here on Seeking Alpha, have drawn a different lesson from this year’s TQQQ price action–that you should only invest in QQQ when stocks are going up.

That strategy was first laid out by investing guru (and noted comedian) Will Rogers on Halloween in 1929:

Don’t gamble; take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.

Good luck getting that strategy to work for you! Bull markets are only obvious when they are almost over.

Leverage Decay Poses Another Well-Known, If Not Well-Understood, Risk

The reason ProShares warns investors that the 3x leverage TQQQ offers can only be achieved for a single day is that when you hold a 3x leveraged ETF for a longer period, a factor called leverage decay kicks in. This is, we are told by ProShares, because the holdings of the ETF are rebalanced daily and the impact of the leveraging used to achieve the daily gain or loss compounds in unexpected ways over longer periods of time, particularly in volatile markets.

The explanations for exactly how this decay might work are extremely complicated and even knowledgeable people will squabble about how exactly it operates. You can read a very detailed explanation of how TQQQ’s leverage decay might work in this mathematically complex Seeking Alpha Article by Warwick Langebrink, who is an investment professional with years of senior level professional investing experience. If nothing else, reading that article should convince you that there is no way you will ever really be able to understand how TQQQ’s decay may behave unless you have taken several years of college mathematics, and even that might not be enough.

What some serious backtesting will tell you, however, is that sometimes the compounding behind “leverage decay” works in your favor. That “sometimes” turns out to be raging bull markets like the one we saw get underway in late March 2020. The unpredictable compounding can compound gains, not just losses.

It is because the warnings about decay damaging returns did not prove to be true during the last two years where QQQ’s raging bull market made for positive impacts from compounding that so many investors are now convinced that decay was not something they had to worry about.

In fact, though, because momentum plays such a big role in TQQQ’s leverage compounding, if momentum turns negative and stays negative, that decay can overtime cause greater losses than that 3x multiplier and high expense ratio and fund trading costs would predict.

Langebrink also tells us that decay will work against us in volatile markets that aren’t heading clearly up or down.

So much for the obvious risks. The more dangerous risks are not these, but others that are rarely discussed. To understand them, we have to examine TQQQ’s stated methodology and holdings.

We Aren’t Given Enough Information to Understand TQQQ’s Methodology

One of the time-tested Golden Rules of investing, one that is right up there with “don’t chase yield” in the list of the Golden Rules that investors keep fooling themselves they can ignore is this: Don’t invest in things you don’t understand. And as we will see, it is the difficulty in understanding what TQQQ is doing that poses its greatest risk.

As investors should always do when considering investing in an ETF, I went to the ProShares website page for TQQQ and read the two prospectuses ProShares provides for this ETF. One is a Summary Prospectus, the other the Statutory Prospectus.

What immediately stood out to me after reading the prospectus is that, unlike what I found in some other Alternative strategy ETFs I have recently investigated, ProShares tells us very little about the actual method it uses to deliver the impressive result its aims for.

We are told that it tracks the Nasdaq 100 Index (NDX), which is the same index QQQ tracks. ProShares also tells us that, “The Fund invests in financial instruments that ProShares Advisors believe, in combination, should produce daily returns consistent with the Fund’s investment objective.” These instruments include:

- Stocks

- Swaps

- Futures contracts

- Treasury Bills

- Repurchase Agreements

They tell us that the Swaps and Futures Contracts are derivatives and that the Treasury Bills and Repurchase Agreements are cash.

Investors, however, are given no insight into how the swaps, futures and cash are used. ProShares tells us only that it uses what it calls “a mathematical approach.” That information is all we get, except for some information about what strategies ProShares does not use. They tell us,

ProShare Advisors does not invest the assets of the Fund in securities or financial instruments based on ProShare Advisors’ view of the investment merit of a particular security, instrument, or company, nor does it conduct conventional investment research or analysis or forecast market movement or trends.

We are also told that though the fund aims to rebalance daily,

The time and manner in which the Fund rebalances its portfolio may vary from day to day at the discretion of ProShare Advisors, depending on market conditions and other circumstances. The Index’s movements during the day will affect whether the Fund’s portfolio needs to be rebalanced.

This statement doesn’t make it clear the extent to which this rebalancing is done opportunistically with human intervention or if it is adjusted by some algorithm.

Warwick Langebrink spends many paragraphs in his article making highly educated guesses as to what TQQQ is doing with its assets, but when all is said and done, they are only guesses.

With TQQQ you are buying an investment you cannot understand. All you can rely on is backtesting, and as the folks who invested in the HFEA strategy learned, 40 years of backtesting isn’t enough to save you if you don’t understand what you are doing. TQQQ only provides us with 12 years.

What are TQQQ’s Holdings?

When I downloaded the list of TQQQ’s holdings as of 5/03/2022 this is a summary of the many line items I found listed:

| Investment Type | Holding | Exposure Value (Notional + GL) | Market Value |

| Cash | 13 Treasury Bills of varying amounts | $4.13 Billion | |

| Stock | The 100 Stocks Held by QQQ in same % Weights as in QQQ | $13.24 Billion | |

| Futures | NASDAQ 100 E-MINI EQUITY INDEX 17/JUN/2022 NQM2 INDEX | $1.39 Billion | |

| Swaps | 13 NASDAQ 100 Index Swaps with Different Investment Banks | $26.40 Billion | |

| TOTAL | $27.79 Billion | $17.37 Billion |

Source: Data from ProShares, Table and Investment Type by Author

The banks involved with the 13 swaps are Bank of America, Barclays, BNP Paribas, Morgan Stanley, UBS, JP Morgan, Goldman Sachs, Citibank, and Societe Generale.

The Stock Component in TQQQ is the Same as in QQQ And Subject to Its Valuation Problems

Since the return of TQQQ multiplies that of QQQ, for future returns to be worth pursuing investors have to believe that the stocks in QQQ still have room to run. ProShares gives us only two valuation metrics for those stocks, dated as of March 31, 2022. At that time the overall P/E ratio of the stock portion of its portfolio was 29.07. The price to book ratio was 8.1. You can find many articles discussing the valuation of QQQ, so I won’t go into that topic in depth.

But as those who follow QQQ know, though it holds 100 stocks, its value is extremely concentrated in the shares of only 10 mega cap stocks, which together as of March 31, 2022 made up 53.70% of the entire value of the ETF. Five of those stocks, Apple, Microsoft, Alphabet, Amazon, and Tesla made up 42.37% of QQQ’s total value. Many of the other 100 holdings of TQQQ are semiconductor stocks.

QQQ also includes a random mix of non-Tech stocks. That is because, by definition, the only factor that the stocks in the Nasdaq 100 index share is that they are the 100 largest cap stocks that originally IPO’d on the Nasdaq exchange. There is nothing that says they have to be tech stocks, growth stocks, or “innovative” stocks though QQQ touts itself as holding “companies shaping the future” and “some of the world’s most innovative companies.” It also holds companies that sell rail freight services, soft drinks, ketchup, and screws.

Given the importance of momentum to TQQQ’s long-term performance, only investors who believe that those top stocks can continue to perform strongly should invest in TQQQ.

The Derivatives Component in TQQQ

Swaps and Futures are defined as “Derivatives” in the prospectus. Most of us have some idea of what Futures represent. But I had no idea what Swaps or “Exposure Value” meant here. So I went and read through some five different definitions of what the term Swap means in an investment context, all of which pretty much said the same thing and did not make much sense to me. A good example is this one from The Corporate Finance Institute:

A swap is a derivative contract between two parties that involves the exchange of pre-agreed cash flows of two financial instruments. The cash flows are usually determined using the notional principal amount (a predetermined nominal value). Each stream of the cash flows is called a “leg.”

These definitions tell us that there are four kinds of swaps, Interest Rate Swaps, Currency Swaps, Commodity Swaps, and Credit Default Swaps. The most common ones are apparently Interest Rate Swaps and Currency Swaps. Nowhere online could I find anything that explained what a swap on a stock index might involve. ProShares’ prospectus for TQQQ repeats the standard definition and only adds this,

The gross return to be exchanged or “swapped” between the parties is calculated with respect to a “notional amount,” e.g., the return on or change in value of a particular dollar amount invested in a “basket” of securities or an ETF representing a particular index.

I don’t think I’m a whole lot dumber than the average investor, but I came away admitting that I have no idea what any of this means.

All I can figure out about the Exposure item is that it is the worst-case amount that the ETF would have to come up with based on its current holding of swaps and futures. And that the exposure is higher than the amount of stocks and short-term bonds held.

Swap Counterparty Risk

Mulling all this over led me to wonder why the biggest investment banks in the world would be selling TQQQ the derivatives that allow it to make such outsized profits. We know these banks are in the business of making obscene gains of their own and we also know that when they do let us little guys get a piece of something that looks particularly juicy there is often a catch.

The answer may lie buried in this wordage buried in the Risk Section of TQQQ’s Summary Prospectus:

… if the Index has a dramatic intraday move that causes a material decline in the Fund’s net assets, the terms of a swap agreement between the Fund and its counterparty may permit the counterparty to immediately close out the transaction with the Fund.

We are then told that if this happens, QQQ could later reverse direction during the day, but investors would still lose out. This could happen in choppy markets and deliver a very different result than what buy and hold investors expect. In fact, backtesting tells us it has probably already happened. As observed in this forum post,

“From 6/1/2011 through 1/31/2012, a $10,000 investment would have made $452 in QQQ but lost -$223 in TQQQ.”

TQQQ Comes With Too Many Unquantifiable Risks

That Counterparty Risk is only one of the non-obvious risks that threaten investors who invest in TQQQ. There are several other risks that rarely get discussed because investors concentrate on price decline risk and leverage decay when discussing the topic of risk.

TQQQ Is A Momentum Play Which Harms Buy and Hold Investors if Momentum Gathers Speed Downwards

Even if counterparties don’t close out their swaps if it looks like they will lose money, the dependence of QQQ’s long-term profitability on upward momentum is a significant risk that the buy and hold investors in these triple leveraged index ETFs wave away.

The many years when QQQ has been relentlessly bullish with only very brief declines that quickly reversed has convinced many buy and hold investors, like the one who wrote the summary I linked above, that TQQQ is safe to hold long term.

The argument they advance that is supposed to clinch this is that even with the dramatic decline in March of 2020 buy and hold investors did just fine. But that argument ignores that the 2020 decline reversed within a week of its March 16 low point and then went on to achieve a once-every-couple-decades gain over the next year and a half.

Leverage decay works in the investor’s favor in an upward trending market. But if a sustained bear market occurs, where stocks reverse course and trend downwards for a year and a half as they did in 2000-2002, the leverage decay will move increasingly against the investor. I took from Langebrink’s article that was cited above the idea that investors will also suffer from leverage decay when the market trades flat but with a lot of volatility, too.

Relying on backtesting is dangerous, as HFEA investors learned whose backtesting assured them that Treasury bonds went up when stocks dropped. Investors who draw their conclusions about how TQQQ will behave based on how it did during a period when QQQ was in a once in a generation bull market that experienced only very short and fast-recovering declines could learn some painful lessons.

Rising Rates Due to Inflation Are Likely to Raise the Costs of Leverage Strategies

TQQQ and other 3x leveraged ETFs have only traded during a period of extremely low interest rates. Rates have already risen and are likely to rise some more. That will increase the costs of any kind of loan, and could very well increase the costs of investing with the derivatives that TQQQ uses.

The Big Banks Who Do Swaps May Raise Their Cost Or Refuse to Offer Them In Poor Market Conditions

Since ProShares warns us that banks may prematurely close their swaps if a single day’s trading goes against them, we would be well advised to consider that if QQQ’s momentum continues to trend downwards, those banks may no longer want to enter into the swaps that TQQQ needs to achieve its goals.

Here, again, we are only speculating because we retail investors can’t begin to understand the motivations of the huge investment banks that sell the derivatives that make TQQQ’s strategy possible. So we can’t really know at what point the cost of their strategy or the inability of ProShares to continue to use it will cause the profits to evaporate–or the ETF to have to shut down.

FINRA Is Exploring “Measures” that May Shut Down or Limit Trading in Highly Leveraged ETFs

I knew early on in my researches that the SEC has publicly expressed its worries about the danger leveraged ETFs pose for retail investors. But it was only when I opened TQQQ’s statutory prospectus that I was greeted on its first page by the following important warning, which I had not seen in ProShares’ Summary Prospectus or other documentation.

RISKS OF GOVERNMENT REGULATION The Financial Industry Regulatory Authority (“FINRA”) issued a notice on March 8, 2022 seeking comment on measures that could prevent or restrict investors from buying a broad range of public securities designated as “complex products” – which could include the leveraged and inverse funds offered by ProShares. The ultimate impact, if any, of these measures remains unclear. However, if regulations are adopted, they could, among other things, prevent or restrict investors’ ability to buy the funds.

This poses a huge risk to anyone who invests in these leveraged ETFs because of the possibility that the ETFs could be shut down or that only wealthy qualified investors would be allowed to trade them.

Restrictions or the shutting down of these ETFs would not be a problem for those who use them to day trade, which, as we saw, is how the company very clearly states they should be used. They could be devastating for buy and hold investors who have built up large positions and are currently sitting on a large loss they assumed would be made good if they were patient and held until the underlying index started gaining again.

If only qualified investors are allowed to trade these leveraged ETFs, they might be a lot less active to the point that they might be closed by the providers as not profitable enough to be worth keeping.

Bottom Line: TQQQ Is Only Suitable For Day Traders Who Use It As It Is Designed To Be Used

Day traders are gambling, but they know they are gambling. If they lose their money, it’s their own damn fault. They could have lost just as much playing the slots.

But the buy and hold investors who have been seduced into believing that TQQQ is a reasonable investment for anyone who believes that the market always trends up over the long-term would be well advised to give TQQQ a pass. If you are already invested and are sitting on a big loss, keep your eye on FINRA’s activities. If they shut the ETF down, you may have to act fast. You can read an interesting article from Charles Schwab about what happened when some other leveraged ETFs were shut down after tanking in April of 2020 here.

Unless you are an investment professional who can explain to me in very simple terms exactly how the investment banks offering the swaps TQQQ uses price those swaps and more importantly what the profit motivation is that makes them want to enter that trade, you’d be well advised to avoid TQQQ except, perhaps as a way to deploy a very small amount of play money you really can afford to see disappear into a puff of smoke.

The issue is not that TQQQ is risky. The issue is that too many of the risks associated with TQQQ are impossible to assess. The unknown behavior of 3x leveraged ETFs due to how leverage decay will affect them in a prolonged flat market or a market like the one that followed the dot.com bust is one set of unknowns. The impact of higher rates on costs, the opacity of TQQQ’s methodology, and the threat of FINRA regulations are others. But mostly it is the inability of average investors to understand the dynamics of the derivatives that drive TQQQ’s excess profits that are most worrying.

Even if those risks didn’t exist, there is the obvious issue that investors have no reason to expect QQQ to experience the kind of dramatic price appreciation it displayed during the COVID-19 lock downs. Without momentum, TQQQ is not an attractive investment. The high expense ratio and the high internal trading costs, which may increase with higher interest rates or flat markets, all work against the likelihood that buy and hold investors will duplicate the windfall profits that were available for the one highly anomalous year when investors trapped at home by COVID spent their spare time gambling on tech stocks.