Goldman Sachs Says Appealing Valuations Make Smaller-Cap Stocks Captivating In this article Are 2 ‘Strong Buy’ Names With Reliable Upside Opportunity

The S&P 500 is up by 14% 12 months-to-date but it has not long gone unnoticed that the strong effectiveness has been pushed by powerful displays from the tech mega-caps.

In accordance to Goldman Sachs strategist Lily Calcagnini, there are much better investment decision opportunities correct now more down the meals chain.

“Small stocks trade at a valuation discounted relative to large caps, suggesting now is an beautiful entry place for buyers with multi-year investing time horizons,” Calcagnini spelled out. “Even within just the significant cap universe, more compact businesses glance cheap relative to greater kinds in the context of both the past 10 and 35 years.”

In actuality, whilst Calcagnini can make the case that the S&P 500 will attain another 9% above the following yr and strike 4,700, she anticipates a 14% increase in the tiny-cap concentrated Russell 2000 index, which will stand for a 5 pp of outperformance vs. the S&P 500 outlook.

In the meantime, the analysts at Goldman Sachs have been getting into the information and trying to find out all those small-caps with sound upside prospective. We ran a few of their picks through the TipRanks database to also gauge popular Street sentiment. Turns out the Goldman industry experts are not the only ones eager on these Russell 2000-integrated names both equally are rated as ‘Strong Buys’ by the analyst consensus. Let’s find out what will make them attractive investment selections proper now.

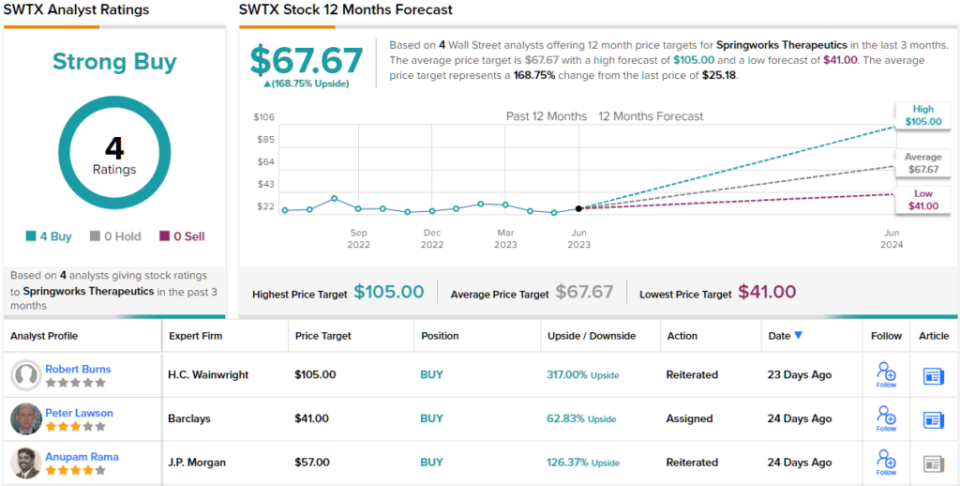

Springworks Therapeutics (SWTX)

Initially up on our compact-cap checklist, we’ll choose a appear at Springworks Therapeutics, a clinical-phase biopharma business with a $1.57 billion industry cap. Springworks uses a precision drugs tactic to receive, produce, and provide transformative medications to marketplace, with the goal of enhancing the life of people afflicted by debilitating cancers.

With biotechs it is all about the pipeline, and Springworks presently has two prescription drugs producing headway in medical trials throughout numerous applications.

The most highly developed of these is oral, smaller-molecule, selective gamma secretase inhibitor nirogacestat, getting assessed as a treatment for various cancers. Primarily based on beneficial details from the Phase 3 DeFi trial, the Fda has acknowledged Springworks’ NDA (new drug software) for nirogacestat in desmoid tumors and a PDUFA day has been set for November 27 (prolonged from the prior August 27 day).

There is another catalyst in the pipeline from the anticipated readout of topline information from the Period 2b ReNeu review of allosteric MEK1/2 inhibitor mirdametinib in NF-1-connected plexiform neurofibroma. This must consider location throughout the next 50 % of the year. NF1 is a genetic condition connected with a heightened susceptibility to tumors, building it 1 of the most prevalent syndromes of its variety. It at this time impacts somewhere around 100,000 persons in the US.

Assessing the pipeline and approaching catalysts, Goldman Sachs analyst Corinne Jenkins highlights the probable of each these drugs: “Based on the accessible medical data, we anticipate a superior probability of acceptance for niro in DT… Additionally, we expect a potent start provided the superior degree of health practitioner awareness and aid for niro in DT noticed across our channel checks and SWTX’s market investigate. Over and above niro, we watch the approaching details from the Ph2b ReNeu study of mirdametinib in pediatrics and grown ups with NF-1-involved plexiform neurofibroma in 2H23 as driving the up coming leg of the tale.”

These feedback underpin Jenkins’ Get rating on SWTX, while her $43 price target implies a single-calendar year share appreciation of ~71%. (To view Jenkins’ monitor record, click here)

Other analysts are even additional optimistic. Of the 4 investment decision banks that have rated SWTX more than the previous three months, all four concur the inventory is a “buy” — and on common, they consider it’s value $67.67 a share — ~169% forward of existing pricing. (See SWTX stock forecast)

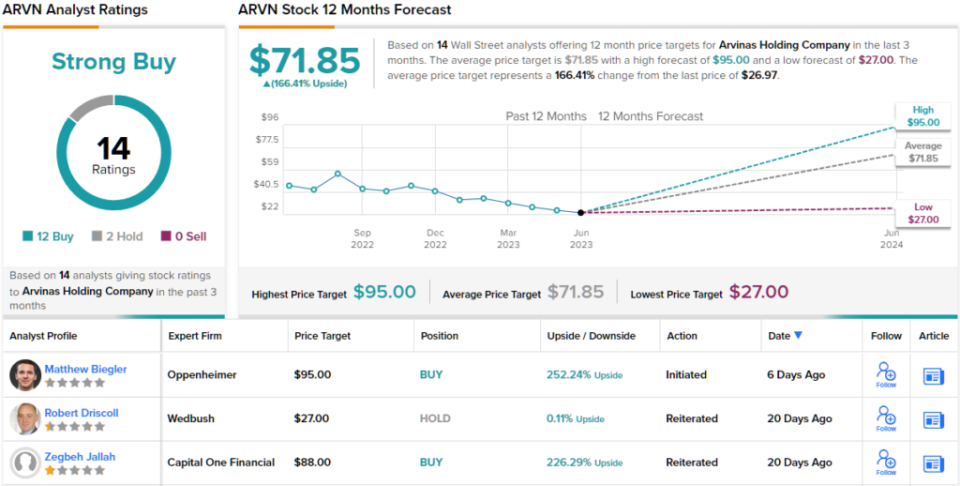

Arvinas, Inc. (ARVN)

We’ll keep in the biotech area for the upcoming Goldman-backed small-cap. Boasting a market place cap of $1.44 billion, Arvinas is a business targeted on building revolutionary protein degradation therapies to handle a large variety of ailments. The firm utilizes its proprietary PROTAC (PROteolysis Concentrating on Chimera) platform, which harnesses the body’s natural protein disposal method to selectively eliminate sickness-producing proteins. By targeting certain proteins for degradation, Arvinas aims to supply far more efficient and durable solutions in comparison to regular small molecule inhibitors or antibodies.

Most of Arvinas’ pipeline is still in the pre-scientific stage but various prescription drugs are in several stages of scientific testing. The most the latest update anxious the development of ARV-766, an investigational orally bioavailable PROTAC protein degrader getting assessed in guys with metastatic castration-resistant prostate cancer (mCRPC). Data from the Section 1/2 dose escalation and growth trial confirmed that ARV-766 was perfectly-tolerated and exhibited promising exercise in a greatly pre-dealt with, put up-NHA (novel hormonal brokers), all-comers affected individual team.

Arvinas is also earning headway in the enhancement of bavdegalutamide (ARV-110), an extra orally administered PROTAC protein degrader. This likely therapy gives a beacon of hope for adult males battling metastatic castration-resistant prostate cancer (mCRPC) who have not responded to earlier accredited systemic therapies. The company is slated to kick off a Phase 3 trial in the latter half of 2023, and intends to disclose the facts on radiographic development-totally free survival from the Phase 1/2 trial within just the very same timeframe.

Irrespective of the abundant pipeline of therapeutic candidates, Arvinas shares are down 21% this 12 months. In accordance to Goldman Sachs analyst Madhu Kumar, this provides an option for the inventory to undertake significant progress.

“Given the early signal, ARVN will progress ARV-766 in mix with abiraterone to pre-novel hormonal agent (NHA) patients in 2H23. Beyond ARV-766, updated info from the Section 1/2 trial of AR PROTAC bavdegalutamide (bav), together with radiographic progression-totally free survival (rPFS), will be offered at a clinical congress in 2H23. Presented the weak spot in ARVN shares YTD, we feel even modest beneficial alerts for the AR PROTAC franchise could produce upside,” Kumar observed.

How does this all translate to buyers? Kumar costs ARVN a Acquire alongside with a $91 value target. Need to the figure be fulfilled, buyers stand to pocket returns of an remarkable 237% a yr from now. (To watch Kumar’s monitor record, simply click right here)

The perspective from the relaxation of the Road is hardly considerably less upbeat. Even though 2 analysts desire sitting this a person out, all 12 other new analyst assessments are beneficial, supplying the inventory with a Potent Acquire consensus ranking. The common target now stands at $71.85, suggesting shares will publish progress of 72% in the months in advance. (See ARVN stock forecast)

To find very good suggestions for shares trading at interesting valuations, pay a visit to TipRanks’ Greatest Stocks to Invest in, a newly introduced software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed in this post are entirely these of the showcased analysts. The articles is intended to be made use of for informational purposes only. It is very essential to do your very own assessment right before building any investment decision.

")