Amazon And Walmart Face Problems With Their India E-Commerce Businesses (NASDAQ:AMZN)

")

Table of Contents

XtockImages/iStock via Getty Images

Amazon.com, Inc. (AMZN) entered the Indian marketplace in June 2013 and virtually immediately entered into a bruising competition with Flipkart (FPKT), which had been operational since October 2007. The latter was acquired by Walmart Inc. (WMT) in August 2018, which reframed said competition into a battle between foreign companies.

Till date, Amazon has invested nearly $6.5 billion into its India efforts and promises to do more in the future. Similarly, Flipkart raised $3.6 billion in funding earlier this year and $1.2 billion in the previous year. Both Flipkart and Amazon collectively claim to control 80% of the republic’s e-commerce space. The battle shows very mixed results from a financial standpoint.

Recent coverage regarding Amazon raised several issues with the company’s leadership and operating structure. The facts emerging from the company’s business in India, altogether ignored by financial media in its home base, lends significant support to this thesis. The consequences of its actions might kibosh its investment in a “growth market” but the financial effect on the company’s top-line items in the immediate term, however, would be limited and interestingly, a substantial positive. The same is true for Walmart as well.

Warning: This article is a hybrid “Long Read”: there’s extensive legal analysis and regulations outlined that Amazon and Flipkart are beset by which is of specific interest to “India watchers”, i.e. the growing class of overseas investors and institutional investment specialists focused on India-specific investments, who wish to understand the landscape.

There are also sections that would be of interest to retail investors holding the stock. Unless preceded by a “Warning” note saying otherwise, the section would be of “common interest” to both sets of readers. Each type of reader can follow the “Warning” labels to read through this article in the most efficient manner.

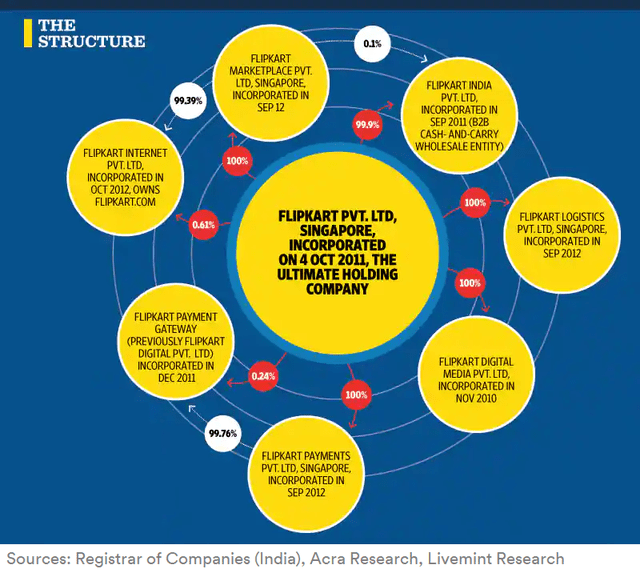

Complex Company Structures

In some ways, Singapore is to India what the Caymans is to the U.S. when it comes to U.S.-listed Chinese “stocks” (which has been discussed before) or, say, the British Virgin Islands is to U.K.-listed stocks.

Comparing Singapore with the Caymans, however, is a bit unfair (as Asian readers will attest). With its name rooted in Sanskrit by way of Malay, the city-state has historically been the trade gateway to India, recognizes the Indian language Tamil as one of its four official languages and is extremely conscientious over its deep relations with the republic. Cooperation between the republic and the city-state have traditionally been on very friendly terms and at levels unique to the East. An earlier article highlighted how Singapore willingly gave up profits on offshore Indian derivatives to avoid a prolonged legal battle with the republic which the former might have won. Both nations immediately turned around and joined hands on an upcoming “Stock Connect” program between the two nations’ exchanges and the world; a stalwart example of classical Eastern diplomacy in the modern age.

The republic allows “foreign direct investment” (FDI) in varying degrees (dependent on sector). To utilize this route, in practice, large companies such as Amazon would incorporate a privately-held “holding company” in Singapore from which cash flows termed “investments” are directed to its privately-held subsidiaries incorporated in India. This holding company could also be transformed into an IPO in the Indian bourses, in which case, the former becomes more-or-less redundant for most intents and purposes.

Amazon has five main wholly-owned companies in India: Seller Services (e-commerce), Wholesale (B2B), Transportation (Logistics), Pay (payment solutions) and Internet Services (AWS). These, in turn, predominantly receive funds from the Singapore-based holding company.

The “multiple companies” structure isn’t unique to Amazon: Flipkart does this too via a holding company in Singapore.

“Flipkart Internet” is the e-commerce arm while “Flipkart India” is the B2B arm. The other names are self-explanatory and correspond with Amazon’s multiple companies in India. Incidentally, Flipkart was reportedly aiming for an IPO in Indian bourses in Q4 2021, which hasn’t transpired yet.

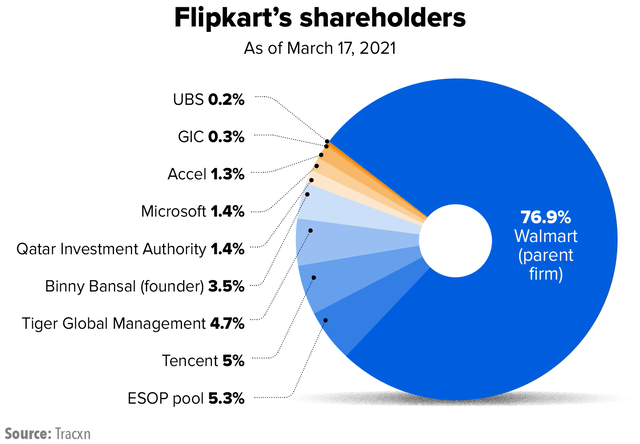

Unlike Amazon, Flipkart is not wholly owned by parent Walmart. There are quite a few major players holding an interest in the company, including the sovereign wealth funds of Singapore and Qatar (in minor capacities).

The Law and Legal Troubles

Since all the “India” and “Singapore” companies concerned are privately-held, they aren’t obligated to release financial reports to the public but do file their annual performance with local regulators (just as with the follow-up coverage given to Mastercard and Visa’s India operations). Thus, given the paucity of public data, analyzing performance becomes a little difficult on a quarterly basis. However, whatever’s available show some very interesting trends.

Note: India’s Financial Year (FY) trails 12 months from the end of March. The financial year technically would be 2019-20 abbreviated to FY20.

Now, Amazon has attracted controversy in the U.S. economy in the past. The argument heard most often against the company, as exemplified by former Treasury Secretary Steven Mnuchin’s statement in 2019, is that the company achieved growth primarily by destroying the U.S. retail industry. (This sort of argument was also made in earlier years about Flipkart’s parent Walmart)

On the other hand, it has also been argued that U.S. sellers’ reach has increased by being on the company’s platform. More arguments abound that the company has decimated more employment avenues than it has created in warehousing and logistics.

Given that there is no empirical long-run statistic currently available beyond surveys, et al, no objective conclusion can be arrived at as to whether Amazon is exclusively or even partially responsible for the current state of small businesses in the U.S. and other “established markets”.

For the record, the Indian government has been very friendly towards foreign e-commerce and retail majors, had even amended the law to allow 100% FDI in e-commerce in 2016 and considers the sector a very cost-effective means for its merchants gaining global exposure. A number of major players have been operating quite peacefully doing precisely that ever since (and even before) the amendment. A few instances:

- eBay (EBAY) was one of the first e-commerce majors to enter the country in 2005 and had a strategic partnership with Flipkart, which ended up buying its India operations in 2017. After Walmart acquired Flipkart a year later, the company quietly re-entered India in 2019 and has been doing rather well since without any hassles.

- Shopify (SHOP) entered India in 2013 and is currently estimated to have a little under 30,000 stores on its platform. No issues here.

- Tesco (OTCQX:TSCDF) entered the country in 2014 through a joint venture with the Tata conglomerate with nary a problem since; the company continues to be a joint venture. So has Starbucks (SBUX) since 2012.

- More recently, IKEA started its India endeavour in 2018 without a domestic partner and there have been no problems.

There are substantial caveats: the law doesn’t allow FDI in e-commerce companies that sell directly to customers. The likes of Amazon and Flipkart are welcomed (and referred to as “marketplaces” in legal language) because they link sellers and buyers. However, marketplaces aren’t allowed to control sellers’ product prices, including on the matter of discounts. The welcome mat to Amazon was publicly confirmed when the republic’s Prime Minister warmly met with and awarded current Executive Chairman Mr. Bezos with the Global Leadership Award in 2016 on behalf of the U.S.-India Business Council.

However, Amazon has been battling numerous lawsuits over the years, particularly from merchant associations who haven’t had issues with the likes of the other platforms mentioned. Flipkart had a few lawsuits from a couple of years before the Walmart transaction but they have increased in fervour after the transaction.

The predominant litigant against both Flipkart and Amazon in the republic’s legal system has been the Confederation of All India Traders (CAIT), which was founded in 1990 and represents 80 million traders’ interests in a rapidly changing republic. The association is well-organized and has been compiling significant volumes of information indicating “malpractices” by foreign e-commerce companies over the past few years.

Another litigant is the All India Online Vendors Association (AIOVA), an interest group for 2,000 marketplace-dependent merchants. This group, while much smaller than CAIT, has been making steady progress in its battle against Flipkart.

Both groups have been making steady progress in “proving their claims” in the legal system.

The government initially was rather blasé about the whole matter, preferring to leave it between the litigants in the courts. In fact, as early as November last year, both central and state governments cleared and facilitated the acquisition of land for Amazon’s AWS segment to set up data centers while Flipkart has been partnered with a government programme to skill and economically uplift underserved sections of its citizenry since 2019. However, since late last year, it’s clear that something was discovered because regulators have now entered the fray with litigation, investigations and more stringent rules being proposed by the government to prevent market abuse in the future from any e-commerce platform.

Warning: The next two subsections are comprehensive deep dives in legal analysis for each company. It’s an important consideration for “India watchers” but other readers can move on to the next section titled “Historical Fiscals”.

Amazon

Note to readers: all relevant publicly-available sources are linked in the text.

On Amazon, two merchants accounted for 35% of all sales until 2019: Cloudtail and Appario. Until March 2016, i.e. the date the law was amended, Cloudtail alone accounted for 47% of all sales. Appario came into existence in 2017.

Cloudtail, as it turned out, was between Infosys (INFY) chairman Mr. Narayana Murthy and Amazon. More specifically, Cloudtail’s parent company Prione was initially a 51-49 venture between Mr. Murthy’s Catamaran Ventures and Amazon’s Singapore-based holding company. Appario’s parent was started by the family that once owned U.S.-listed Patni Computer Systems under the exact same terms.

What set the ball rolling were leaked documents accessed by Reuters from Mr. Jay Carney, Senior Vice President at Amazon, one-time press secretary for President Obama, the manager of a group of about 250 registered lobbyists (as of 2021) for Amazon and, of course, a past winner of the Gerald R. Ford prize for distinguished reporting. In these documents, the modus operandi and goals were set for these two sellers, dubbed “Special Merchants” (SM1 and SM2, respectively).

In these documents, the stated goal was to make SM1 (Cloudtail) a $1 billion+ business by 2015 and be responsible for 40% of all sales. This goal was met in spades. The modus operandi was thus: the most popular items in the marketplace were offered by the “SM” at a price programmatically made lower than other popular merchants’ while having special privileges such as listing placement and discounted/free shipping. If the product offered was unique, the company would engage a manufacturer to replicate the product and then offer that at a lower price. Some of these products were also offered as “Amazon” brands under labels such as Solimo, SymActive and, of course, AmazonBasics.

The 2016 law required that a level playing field be offered to all participating merchants and that no single seller can ever have more than 25% share of sales. Among the terms of the “level playing field” defined was that there should be no significant business relationship between the marketplace and the seller. Subsequent to the 2016 law, “SM2” (Appario) joined the marketplace.

After the news broke, both SM1 and SM2 departed the company’s platform and the company reduced its holdings in both to 24%. In a surprising move given the legalities, both returned to the marketplace after this. News emerged in August this year that Catamaran and Amazon would be ending their relationship by Q1 2022 and Cloudtail would cease operations. In yet another baffling move, the company reached out to regulators on December 22 asking for permission to buy Prione and informed the regulators that Prione will keep functioning (i.e. selling products on the marketplace) until regulatory approval. Once again, the law clearly states that companies such as Amazon and Flipkart can only perform as marketplaces and not own a seller.

There have been a number of such baffling moves by the company over the past couple of years. In 2019, the company bought a 49% stake in Future Coupons, a reward points and customer loyalty program operated by Future Group for about $200 million to promote “buy-ins” into the marketplace’s payments service. The latter can best be thought of a mid-sized Walmart with about 1,500 stores of various sizes and a relatively modest digital platform. At the time, the investment was deemed to be equivalent to a 3.58% stake in Future. In 2020, however, Reliance Retail, which operates over 12,000 stores and has a rapidly-growing digital platform, finalized a deal to acquire debt-stricken Future Group for $3.4 billion.

Amazon immediately went to sessions court on the basis of a non-compete clause in its agreement with Future, which ruled that the clause was with a subsidiary (“Coupons”) and not the company itself. The company then went to Singapore’s arbitration system (because Future had a holding company there) which halted the proceedings. Future took the case to the High Court in India where its attorney, Mr. Harish Salve, pleaded, “Please don’t allow this American giant to kill Future Group only to further its illegitimate interest to make sure that Reliance does not get its hands in. That’s its game plan—if I can’t get it, let Reliance not get it too.” The court was unmoved and found the Singapore arbitrator’s ruling valid.

Undeterred, Future approached the antitrust tribunal, a specialized court for corporate affairs, which re-examined the facts and found the case suspicious. Amazon’s counsel tried to stall the proceedings by demanding a postponement. The tribunal ignored this demand and the company’s counsel staged a walkout. India is no stranger to the idea of Civil Disobedience; Future’s counsel called it an attempt to browbeat the tribunal, the tribunal seemed to agree and allowed the sale to proceed.

Now, the company’s stake in “Coupons” entitled it to about $122 million as per the Reliance-Future deal which, given the fact that Future was a loss-making entity with a further billion dollars lost during the pandemic in 2020, would have been a pretty decent recoup in investment. On December 17, the antitrust regulator found that the company had suppressed information (likely because an investment in a coupon program for a payment platform was made to imply partial ownership in a retail company and its other assets) and dissolved its 2019 assent to the investment until further review and imposed a $27 million fine. In the latest update from December 23, the company has sued the republic’s financial crimes investigation unit because the latter, suspecting that the deal with “Coupons” violates FDI laws, has been interviewing the company’s India-based executives.

There’s more: there may be another reason for this case.

As is clearly discernible, the company has been burning cash in numerous lawsuits with various courts and arbitration systems in India and Singapore. Across FY18 and FY19, the company’s audited statements to the Indian registrar of companies had recorded a sum of approximately $285 million paid for “legal professional services”. News emerged in September that compiled filings with the companies registrar shows that the total sum paid in legal and professional fees in FY18 through FY20 was $1.2 billion, making the FY20 sum around $921 million, which is more than what the biggest law firm in India earns in a year with a full roster of clients.

The company rapidly denied that this was the case and claimed that only a $7.3 million were legal fees while the rest was paid to professional consultants: customer research, advertising, marketing, etc. This was refuted by a number of legal and accounting professionals since many of these were separate line items already filled in. Litigant CAIT accessed the audited statements filed with the government and revealed that total legal and professional consulting expenses from FY18 through FY20 was to the tune of $740 million.

The company’s attorney was sent on leave just as a whistleblower reported to authorities that legal professional fees paid out are used to bribe public officials. This isn’t just a crime in India; it’s a violation of the U.S. Foreign Corrupt Practices Act. The punishment in both countries is prison time: up to 7 years in India and 20 in the U.S.

The $7 million amount for FY20 also brings up an interesting point: high expenses are repeatedly seen in prior years’ filings with regard to professional consulting services, advertising, et al. Government sources indicated to the media in September that they’re investigating the matter but had declined to expound further.

As mentioned before, government actions in the past indicated significant bonhomie with and support for Amazon’s India endeavour. But now, with leaked documents, whistleblowers and the company’s suspicious legal maneuvering, it’s very likely that the republic’s various investigation units are currently digging deep.

Flipkart

Note to readers: all relevant publicly-available sources are linked in the text.

In FY18 and FY19, i.e. immediately after the Walmart acquisition, the company has spent nearly $90 million in “legal professional services”. The antitrust investigation into Flipkart had been dismissed by another court before a request to resume proceedings was filed by CAIT. Flipkart is represented in these proceedings by Mr. Harish Salve.

In the latest round of arguments in June, CAIT alleged that the platform forces sellers to cut their prices in a bid to boost sales without offering compensation. At which point Mr. Salve said, “I tell my sellers at a time like Diwali if you reduce your prices, I will give you a reduction in rent. What’s wrong?”

CAIT immediately proceeded to seize upon this statement by highlighting that FDI policy states that a marketplace cannot dictate prices to merchants.

This “dictating prices” argument made by CAIT against both Amazon and Flipkart is related to their “deep discounting” sales growth strategy, which creates a tax issue as well as a legal issue. First of all, it bears noting there are two levels of sales tax: the Central (which is lower) and the State (which is typically higher).

Here’s how the discounting/taxation process works for almost every e-commerce platform.

Firstly, the discounting: the platform compares prices of a product in other marketplaces and recommends a discount amount (the amount the price is to reduced by) to that product’s seller on the platform. The platform finances the discounts. The product is sold at the suggested price and the platform keeps its cut, i.e. the commission/listing fee.

Second, the taxation: This is a little different between platforms. At the end of a certain period (say the end of the month), the seller sends a debit note to Amazon titled “promotional funding” which contains the discount amount plus the service tax on that amount. The company pays this note (plus a small discretionary extra amount) to the seller. The seller pays the central service tax to the government.

For a seller on Flipkart, discounts are not funded by the company. The company instead forgoes the commission/listing fee.

This is a problem: for e-commerce transactions, sales tax is collected based on the product’s cost price (i.e. the price at which the seller purchased the product) and then on the sale price to the final customer. If the product is sold below the cost price, then the tax collected from the customer is much lower than what was paid originally. In this case, the seller would be eligible for a tax refund from the state tax department they fall under.

When it comes to Amazon, the seller pays the central sales tax on the discount amount and the state tax on the rest. But if treated as a whole, there are many cases when sellers are eligible for a refund from the state but cannot collect it.

In either case, the CAIT maintains that prices are dictated, in that the seller has no option but to accept the discount. More interestingly, the CAIT has stated since 2019 that it has comprehensive evidence of this on both companies.

With regard to Flipkart, the company had a “Cloudtail” problem until recently too: until about 2014, the seller “WS Retail Services Ltd” accounted for 75% of sales on the platform (and didn’t receive a discount refund). Until 2012, this seller was owned by the founders of Flipkart until a financial crimes investigations unit started a probe. The seller finally stopped selling on Flipkart in September 2018.

There have been a handful of other complaints on Flipkart such as:

- A discontinued product was advertised as available on the platform followed by an inducement for users to join and shop, which a marketplace cannot do (example: eBay India doesn’t advertise at all. Despite that, it has 30,000 merchants selling to 2.1 million shoppers in India).

- A top executive whose services were terminated has been threatening to go to court and “reveal all”.

- Both companies are in trouble for not adequately labelling the point of origin of goods. This is partly needed due to the rising boycott of Chinese-made goods by citizens (that the government’s elected representatives have been encouraging) but primarily a regulatory requirement.

These issues are relatively minor compared to the one late last year: an order was passed by the antitrust tribunal directing an investigations unit to conduct a probe into the platform based on a complaint by AIOVA that the platform was abusing its dominant online position. The tribunal found sufficient evidence to initiate proceedings against the company.

Mr. Salve approached the Supreme Court on a technicality: a separate antitrust unit had found the platform’s position to be not dominant; ergo, there is no cause for complaint and there is no market abuse. The Supreme Court was keen to send the matter back to the tribunal but the original complainant stated that they’re prepared to make their case before the Supreme Court. So, the tribunal’s decision was stayed and arguments have begun afresh.

In news as of August this year, the financial crimes investigation unit sent a notice to Flipkart asking why they shouldn’t be fined $1.35 billion for violating FDI rules.

Historical Fiscals

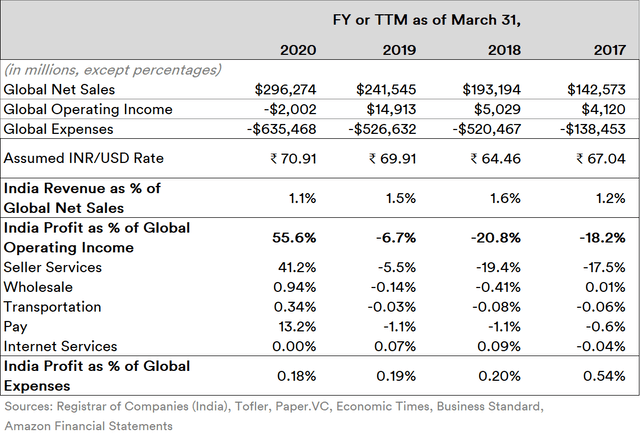

Now, given that the financial calendars are different in India and the U.S., the India fiscals are from the audited statements submitted to the registrar while comparative U.S. numbers are from the unaudited Trailing Twelve Months (TTM) covering the same period. Generally, it has been determined that there isn’t a significant difference post-audit most of the time.

An average annual rate for currency conversion is estimated for each FY using the daily USD/INR spot rates in London currency brokerages to smoothen the evaluation.

Going over from FY17 to FY20, the highest contribution from India operational revenue to global net sales has been well under 2%.

Given that the company’s operations have not drawn a profit till date, a comparison of negative (i.e. outflow) vs negative shows that it’s well under 1% of the company’s total expenses.

On the downside, however, the particularly large representation of India “profits” in FY20 isn’t a profit. In the TTM, the global operating income was at a loss of $2 billion – a little over half of which was from its India operations. The Pay segment is a relatively recent addition, so it is left aside. As a whole, though, “India” losses have dragged down the operating income every year.

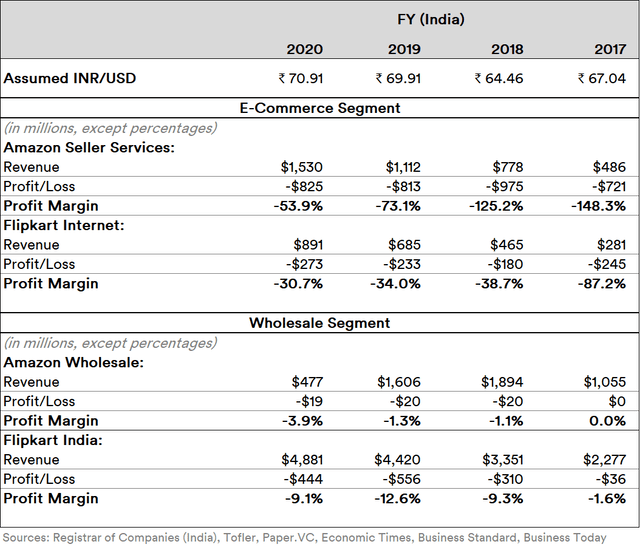

Comparing the performance of the two historical main segments for both Flipkart and Amazon in India, i.e. e-commerce and wholesale, reveal some interesting trends.

While neither company shows a positive profit margin in either segment, it can be seen that Flipkart’s e-commerce segment does relatively less badly while Amazon’s wholesale segment does the same.

Final Notes

Warning: The following subsection is of interest to “India watchers”. Other readers can move to the next subsection titled “Amazon/Walmart watchers”.

India Watchers

As the dissection of rules and events show, both Amazon and Flipkart seem to be outliers in the legal challenges they face, when considering that other e-commerce/retail companies (both foreign and domestic) seem to be operating quite comfortably in this “regulatory landscape”. Thus, it’s possible to conclude that, based on the facts presented, the challenges with the “landscape” are uniquely derived from these two players’ highly-similar “operating style” in India.

When it comes to e-commerce/retail, the “Inventory-Based Model” e-commerce/retail blended company to watch for would be Reliance Retail, whose listing is eagerly anticipated. It’s possible that the company might list in the Indian bourses either around or after the Indian bourses’ “Stock Connect” programs start operations in 2022. In any case, the company has indicated that it will be doing so within five years.

In “pure play” e-commerce, Tata conglomerate-owned BigBasket is a beast, with roughly 35% of the e-grocery market cornered two years ago and growing since. Post-acquisition, all but one of the founders have stayed on and either the company or its parent Tata Digital is aiming to list in 2023 after expense line items start trending positive. Tata-owned companies typically never list abroad; the republic is their turf.

Both companies are expected to have bumper listings and add to the growing list of successful IPOs at the National Stock Exchange (NSE)/Bombay Stock Exchange (BSE) in India in recent times. A recent article that discussed the Paytm (PAYTM) IPO at the NSE highlighted how “Wall Street”-styled analysts couldn’t even model the landscape while Dalal Street’s street-smart traders ate the former’s lunch by utterly rejecting the proposed valuation. In fact, the closing price as of December 23 is 37% lower than the issue price of ₹2,150 and finally received a bullish signal from Morgan Stanley on December 22 after gaining approval to effectively become a bank for foreign fund transfers. However, even the target price remains lower than the issue price.

Wall Street houses’ India analysts often bemoan that the Indian equity market is “too conservative”, but Dalal Street has come a long way in the past 30 years; it simply doesn’t (and needn’t) kowtow to Wall Street-style hoopla on its turf.

That wasn’t even the last time Dalal Street got one over Wall Street: on December 21, CE InfoSystems (better known as “MapMyIndia”) had a listing debut on the Indian bourses with a 53% premium over issue price and was oversubscribed by 154.7 times the number of shares. Institutional houses (also termed “HNIs”) allegedly started panic-selling the very next day, which didn’t fool Dalal Street: they correctly read the positive fundamentals of a debt-free and heavily specialized company that’s been around for nearly a quarter-century. As a result, traders and retail investors bought up premium-value shares at a discount and are currently bullish on the stock. As the aforementioned coverage on Paytm indicated, there seems to be a massive knowledge gap in Wall Street when it comes to Eastern equity markets.

There are also upcoming restrictions being mulled by market regulator SEBI aimed at “managing” algorithmic trading – currently a significant playpen for “Wall Street”-styled houses and a massive intraday volume driver in Indian bourses with short- to mid-term trend implications on stock performance – which is audacious and innovative. Innovation drives the East: that entire matter would be a “deep dive” on its own and might be covered later as a standalone article, if work commitments allow the time for it.

Amazon/Walmart Watchers

Both companies (as well as market commentators) sometimes state that their India operations are navigating a “challenging regulatory landscape” which, while partially true, omits the fact that there were aspects in their operations that might have escaped due diligence for any number of reasons. In the aforementioned leak of Amazon Vice President Jay Carney’s files that was accessed by Reuters, Amazon’s top leadership seems to have instructed its India managers in a presentation to “actively test the law” and be prepared for “dawn raids” by regulators.

There is some support to the idea that both Amazon and Flipkart tend to “lead each other” in their India plans in the course of their long-standing competition. The “deep discounting” growth strategy pursued by both platforms to enable rapid sales growth might have exacerbated to the point that sellers were forced, like the CAIT and AIOVA claim, to accept discounts at their cost. For the record, both litigants appear to be very confident about their evidence and have offered the same to virtually every regulator, tribunal and investigation unit in the republic. Given the long list of issues and purported violations, it’s highly unlikely that it will be “business as usual” for these specific foreign players in India. As of August this year, the country’s Supreme Court has dismissed the plea by Amazon and Flipkart to squash antitrust investigations against them and has directed the investigation unit to proceed.

Note: In coverage given to Sea Limited (SE), it was mentioned that the company’s Shoppee platform was entering India. CAIT has already investigated the parent company’s India-facing structure, listed the specific violations of FDI norms and highlighted its links with a Chinese tech company banned in India (which was predicted to be an issue in the coverage) in its request sent to the Ministry of Finance on December 16, asking that action be taken against the company.

India is by no means an outlier: Chinese e-commerce giants Pinduoduo (PDD) and Meituan (OTCPK:MPNGF) were fined in March specifically for excessive discounting. Furthermore, trends seen in public commentary in the rest of the East indicate that, in virtually every “growth market”, there is significant popular (and thus governmental) preference for indigenous e-commerce players engaging with indigenous merchants. This is fine from an investor’s perspective: a larger number of e-commerce tickers adds choices for investor portfolio diversification strategies.

There was no fiscal comparison between Walmart and Flipkart like with Amazon for a simple reason: the latter is an investment held by the former. In fact, Walmart’s annual report for FY21 states that “Flipkart’s result of operations since acquisition and pro forma financial information is immaterial”. There is virtually no cross-linking between the two companies’ catalogues. The current problem with Flipkart’s listing plan is possibly because it intends to pursue an “Inventory-Based Model” in the future by having its own products in the catalogue, which it cannot as per FDI rules.

Let’s assume the worst-case scenario and model it as a pure “back of the envelope” calculation: Walmart has to divest completely so that the Flipkart IPO can go up on Indian bourses in Q2 2022. In September 2020, Flipkart as a whole was reportedly valued at $50 billion. As of July this year, it was valued at $37.6 billion. Let’s assume this valuation doesn’t change. Assuming that there will be plenty of buyers for the stake – ranging from Indian conglomerates other than Tata and Reliance to sovereign wealth funds and Indian investment houses – and subtracting the $1.2 billion in funding given to Flipkart earlier, the resulting sale would net Walmart about $27.4 billion, i.e. a cool 71% premium on an investment held over 3.5 years. Not bad at all.

To put this in context, Walmart has 2.77 billion shares outstanding and has announced that the annual cash dividend for FY22 would be $2.2, the 48th consecutive year of dividend increase. The payout value from the sale of stake in this subsidiary of “immaterial performance” is nearly 4.5 times the present dividend outlay. Of course, as the annual report indicates, this acquisition was financed by an issuance of notes. Thus, the sale proceeds could potentially be used to pay off the notes earlier or be invested into its significantly-more successful business in its “established markets”.

Amazon has always offered the idea of “growth” to its investors but this isn’t necessarily possible only through geographic growth. The company has already established near-ubiquity and largely stabilized its margin trends in its “established markets”. There is plenty of solid potential for it to enable faster growth by shifting focus to newly-developed service offerings. Outside of one U.S. Senator, possibly due to its extensive network of lobbyists under Mr. Carney, there is virtually no support for any action on the company among either regulators or elected officials in its “established markets”.

If the company were to exit India, there is no recourse for a neat “brand” sale like Walmart. However, the company’s stake in its physical/logistics network (i.e. literal real estate) could likely hold accrued value, although most of its real estate would likely be long-term leases. Also, the trends in fiscals indicate that while revenue and expenses won’t be heavily affected by an India exit, the effect on operating income would be wondrous. The resulting boost would substantially improve both overall efficiency ratios and stock valuation for years as well as maybe leave enough for a dividend payout for investors, which it has never done in its 24 years. The company’s getting a little old to be doing lines and hitting the town like it’s a “growth stock” in 1999. In its quest to compete with Walmart, it makes sense to start paying the bills like Walmart.

The company’s AWS endeavour faces an uphill battle due to the data localization measures being considered in India (and in the works at every major nation) that would likely inhibit it from optimizing efficiencies of cost in the near term. Indigenous data warehousing and value-added services providers are rising to the occasion but they’re massively focused on – and positioned to profit from – long-term growth in India. In any case, AWS in India has historically been rendered a minor player by the company itself, despite showing comparatively better performance (i.e. its trends are generally positive or near-zero when all other segments were negative). Exiting the “marketplace” and refocusing on this segment would likely provide stronger returns to the company as well.

In conclusion, as far as both companies are concerned, it’s a peculiar twist on the “cutting losses” trope: both companies’ stock are likely to get a boost by doing so. If market sentiment turns bearish if/when they do, it would present an interesting “buy the dip” case for those bullish on these two stocks.

As far as Amazon is concerned, many of the facts presented seems to confirm what prior coverage had opined: management’s priorities seem to be quite muddled. Given present ownership patterns, there’s simply no means for investors to nudge the company into not throwing good money after bad and switch to either rewarding cash to its investors or pursuing faster growth in alternative offerings in “established markets”.